Financial responsibility of a father

Financial Responsibilities of Fathers | Christian Credit Counselors

May 12, 2015

What role do you play in your household? What are your responsibilities? For more than seventy million fathers in the United States countless responsibilities are assumed, especially when it comes to the well-being of their family. Even though many households today consist of two-income families, a lot of the financial, physical, and spiritual stress can fall on the man of the house. After all, who taught you how to ride your first bike? Who was there to make it all better when you fell and scraped your knee? Who took you to the daddy-daughter dance at your school or church? Who taught you how to throw a baseball? Who tucks the kids in bed and kisses you good night? Not only can fathers and husbands be looked to for being strong role models that provide the significant mental and emotional pillars of love, guidance, security, support, and wisdom but they also take on vast financial responsibilities as well.

Today, it’s estimated that Americans spend over one billion dollars each year on gifts for Father’s day to show their appreciation for taking on these responsibilities and providing for their family… but what does a FATHER spend on HIS family for the other 364.5 days of the year? According to the newly released estimates from the U.S. Department of Agriculture, it will cost a middle-income couple $245,340 to raise one child born in 2013 to the age of eighteen and this doesn’t even include the cost of college! Of course, this amount can vary widely depending on location, income, and number of children in the household. Nevertheless, let’s take a look at JUST A FEW things that a father may be financially responsible for providing to his family:

- Basic Needs- food, water, clothing, housing

- Health care- insurance for family/dependents

- Child care and Education- day care, tuition, educational materials, transportation

- Future Security- college tuition, retirement, will or testament to family, life insurance

- Miscellaneous- transportation, lessons, leagues/teams, concerts, vacations, trips, toys, candy, ice cream, gifts, video games, technology, etc.

You must admit, these are FAIRLY important aspects in life (food, housing, AND CANDY) and this list only scratches the surface of responsibilities that a father may undertake as an important contributor or head of the household! Father’s Day is a time to say thank you to fathers who accept all of these duties and more. So how can we repay them? Remember, saying “thank you” is free of charge but is a simple phrase that can be worth more than you know! How will you celebrate Father’s Day?

Do you want to know more about debt and how you can make smart financial decisions now that will help you secure a more prosperous financial future? Sign up for our newsletter for monthly money tips.

Full Name (required)

Email (required)

Are you a current client of Christian Credit Counselors? (required)

---Yes, I'm a current client.No, I'm not a current client.

Type the code below in the text box. (required)

Resources: www.history. com, www.money.cnn.com

com, www.money.cnn.com

Fatherhood, Money & Providing for Your Family

Providing financially has been a key aspect of fathering through the ages. Until about half a century ago, almost all that was expected of a father was to protect and provide for his family. Today, most men realize that the cultural perceptions are changing: a good father also communicates with his children, expresses love for them, and is involved in many aspects of their lives.

This is progress, but we must not lay aside the importance of financial provision as a key part of effective fathering.

A committed father is compelled to contribute to his children’s well being—whether he’s a non-custodial father faithfully paying child support, a working father in a more traditional situation, or an at-home dad who takes care of his children while his wife earns the family salary. Financial issues bring meaningful opportunities to the fathering role; our task is to make the most of those opportunities.

Finding a Balance

We want to be good providers, but not be consumed by the pursuit of income or a workaholic lifestyle. If a dad is convinced that providing for his family is important, he might throw himself into his work at the expense of time at home. Before long, his relationships with his children start to wither away.

Our research shows that the most effective fathers don’t necessarily have the highest income. The level of income is not as important as a steady income that meets the family’s needs. An “A+” provider can have a “C” income. In this case, “average” is sufficient.

When a dad adopts this perspective, he is free to make career decisions based not on his neighbor’s lifestyle or his company’s standards, but on his life goals, his family’s needs and his children’s future. He’ll probably feel less tension between home and work responsibilities, and he’ll be free to turn down opportunities that promise more money but also demand more overtime.

Too many dads are waiting to meet certain financial goals, then they’ll spend more time at home. But often, when they reach their goals, they have established patterns at work and at home that are very difficult to change. And while they’ve been off working long hours or cutting big deals, their relationships with their kids have withered away. When they do decide to focus more on their families, there is often a shocking and sad recognition of what they have missed—and can never recover.

If you’re seeking “the good life” by pursuing wealth, you’re on shaky ground. No matter how much money you have, the best life comes from well-connected relationships. Providing well for your family means bringing home a paycheck, and it means bringing home a lively, caring, engaged father.

Planning for the Future

Wise financial management is all about anticipating and preparing for the future. So is wise fathering. Finances impact fathering in two important areas:

1. Handling the costs of today and tomorrow. Children bring many expenses to the family budget, and as they grow, so do the costs. The everyday expenses are easy to remember, though not always easy to pay. Many of them are ever-present: we’re very aware of how much we spend on diapers, clothes, food, summer camp, oboe lessons, child care, doctor’s bills, more clothes, and so on. But in our efforts to keep up with the everyday expenses, it’s easy to neglect important long-term goals. Or worse, in our consumer-driven culture, many of us go into debt because we want to increase our standard of living now, and in the process we’re mortgaging our future and our children’s future.

Handling the costs of today and tomorrow. Children bring many expenses to the family budget, and as they grow, so do the costs. The everyday expenses are easy to remember, though not always easy to pay. Many of them are ever-present: we’re very aware of how much we spend on diapers, clothes, food, summer camp, oboe lessons, child care, doctor’s bills, more clothes, and so on. But in our efforts to keep up with the everyday expenses, it’s easy to neglect important long-term goals. Or worse, in our consumer-driven culture, many of us go into debt because we want to increase our standard of living now, and in the process we’re mortgaging our future and our children’s future.

We can’t predict the future, but we can anticipate that certain expenses will come along at particular stages in our children’s lives. And we can anticipate that providing will only get more costly as our children grow. They’ll eat more food, wear out or outgrow more clothes, be involved in more activities, and need more equipment, health care and transportation. We need to plan wisely if we’re going to keep up.

We need to plan wisely if we’re going to keep up.

That’s also true when it comes to our children’s economic future. An effective father knows what his child’s plans and dreams are and provides steady affirmation of those plans and dreams. Eventually, he may help provide the necessary education to support those dreams.

There are few gifts that are better for a father to give than an opportunity for a good education. Each family should agree on the approach that works best. Some parents, by plan or by necessity, require their kids to pay some or all of their college expenses; others save so they can foot the entire bill. Whatever your family decides, start preparing now. Use time and interest to your advantage.

Finally, preparing for the future should include life insurance, a valuable tool that provides for your family in the event of your death. Before you had children maybe you had an argument for not needing it, but as inexpensive as many policies are, there are no good excuses for leaving your family unprotected.

2. Teaching kids to handle money. We can never start too early. We need to talk with our children about money and model the right attitude about it.

One approach you might consider is sharing some financial matters with the entire family. What better way to teach your children than to let them watch you make decisions? You might even try turning a month’s wages into cash, so your kids can see how it’s divided among the various expenses. They’ll get a better understanding of your family’s limited resources and just how much it costs to run the air conditioner, feed the family, buy school clothes, etc.

Have a clear vision of what attitudes you want to teach and model for your children. Some good ideas might be: hard work, being content with what you have, delaying gratification, planning for the future, and practicing patience and perseverance.

Keep in mind that it’s important for your children to have money to manage. There are so many important life skills and lessons related to finances, and the goal is to let your kids learn a lot about money at a young age with small amounts, knowing that those lessons will continue to be valuable later in life, when the costs and the stakes are much higher.

There are so many important life skills and lessons related to finances, and the goal is to let your kids learn a lot about money at a young age with small amounts, knowing that those lessons will continue to be valuable later in life, when the costs and the stakes are much higher.

How will they get that money, and how will they manage it? Here are five principles that you will probably want your children to learn:

1. Earn diligently. Earning money gives your child a sense of worth. Young children need to know they can make a valuable contribution and they have marketable talents, even if the current market is only in your kitchen or backyard.

This brings up a question that every father or couple will need to answer: Should your children earn all the money they get, or should you give them an allowance that isn’t tied to chores or other jobs around the house? Or some combination of the two?

Of course, the “earn what you get” approach has merits for many. Other parents provide an allowance so their kids can start learning those important life lessons, and they build in the expectation that their kids will carry part of the family workload without pay–and they’re free to earn additional income by other means. Use the approach that matches best with your values and priorities, or perhaps what makes sense because of your childhood experiences.

Other parents provide an allowance so their kids can start learning those important life lessons, and they build in the expectation that their kids will carry part of the family workload without pay–and they’re free to earn additional income by other means. Use the approach that matches best with your values and priorities, or perhaps what makes sense because of your childhood experiences.

2. Save consistently—even if it’s just a little bit each month. Kids will marvel at how their accounts grow as a result of their modest but consistent savings plan. If your child learns to save something each time he gets some money, he has learned a valuable lesson that many in this generation have lost.

3. Give cheerfully. Early in life, children should learn the satisfaction of helping others.

4. Spend wisely. Whether they are spending money they have earned or spending an allowance, there are important lessons to be learned. It’s amazing how fast kids learn the difference between a wise investment and a waste of money when they’re spending their own dollars—especially when parents don’t bail them out of unwise decisions.

5. Receive graciously. Our joy in giving is multiplied because we know the pleasure of receiving. For some of us, receiving is uncomfortable because we don’t like to show any need or weakness. But our children need to learn that using the phrase “thank you” demonstrates strength, not weakness.

Being a Dad … Priceless

According to the U.S. Department of Agriculture, a middle-income married couple whose child is born in 2015 will spend $284,570 (with inflation) to raise that child to age 18. That’s over $15,000 per year, $304 per week, or $43 a day.

What did we get ourselves into? A financial advisor might look at those figures and say, “Don’t have children if you want to be rich.” Actually, it’s just the opposite.

How can you put a price tag on feeling a child move inside its mother; hearing your new baby let out that first, glorious wail; or hearing “Da-da” for the first time?

What do you get for your $284 grand? How about a sticky hand to hold; a partner for blowing bubbles, flying kites, building sand castles, and skipping down the sidewalk; someone to laugh yourself silly with, no matter what else may have happened that day; and glimpses of God on a daily basis.

You invest all those thousands, and you never have to grow up—you get to finger paint, watch cartoons, play hide-and-seek, and catch lightning bugs. You’re a hero for retrieving a Frisbee off the roof, fixing a bicycle, or removing a sliver. You get a front-row seat for the historic first step, first word, first day at school, and first time behind the wheel. You get an education in psychology, nursing, criminal justice, and communications that no college can match.

You have the power to heal boo-boos with your kisses, scare away monsters under the bed, patch a broken heart, and love your children without limits. And, if you’re so blessed, one day they will return your love without counting the cost.

What do you think, dad, are kids worth all that cash? If we adapt the old credit card ads for fatherhood: being a dad might be costly, but the experiences are priceless.

What insights would you add? What’s your #1 tip for providing for your family and maintaining the right perspective on money? Please leave a comment and encourage other dads on our Facebook page.

.

what are the obligations when they have to pay alimony

According to the law, parents have obligations in relation to their children. Does the other party have responsibilities for caring for parents, and if so, what are they? Not in terms of morality, but legally.

I think that my father did not raise me in the way that is necessary for the normal development of a person, therefore I am not going to help and communicate with him in this life. What difficulties may arise, how can I be held accountable? Inheritance does not interest me.

A.

By law, able-bodied adult children are required to support and take care of their disabled, needy parents - to pay child support. Disabled parents are parents with disabilities or women over 55 years old and men over 60 years old.

Alisa Markina

lawyer

Author profile

But not everything is so simple. If you do not want to voluntarily pay child support, then the parent must demand it through the court and justify the amount. To come and say "Let's give me 15 thousand every month" will not work.

To come and say "Let's give me 15 thousand every month" will not work.

As I understand it, you are also wondering if you need to do something for your father: cook, wash, clean. This, of course, is implied by the duty to care, but in practice children are not forced to actively help their parents and communicate with them - you don’t have to worry about this.

Responsibilities of children towards their parents

There are quite clear conditions in the law when adult children must financially provide for elderly or sick parents. In short:

- Children of full age and able to work.

- Children have the financial ability to help their parents.

- Parents objectively need money to survive and cannot get it from someone else.

- There is no evidence that the parents did not take care of the child in childhood.

st. 87, 88, 169 SK RF

If you do not want to pay your father money for maintenance, he can demand it from you only through the court. To do this, he will have to file a claim for alimony.

To do this, he will have to file a claim for alimony.

So what? 03/22/19

Alimony for pre-pensioners: who will pay and how to get

Alimony can be collected only for a maximum of three previous years. And then, if the parent proves that he tried to get money without a trial and turned to you with written demands.

Art. 107 SK RF

How parents can get money from the state

We’ll tell you in the free Glass of Water mailing list: once a week we send a letter about the financial side of parenthood

Circumstances taken into account by the court

If you live an ordinary life without a huge income, and your father does not have serious illnesses, the court may not collect child support from you. Or collect them in a symbolic amount. There are many factors that affect the amount of alimony - we have already written about them.

Art. 98 SK RF

Thus, the court must take into account what income and property the father has. For example, if he receives a pension, the court may consider that the father is provided for anyway. The regions automatically raise the pension to the subsistence level for pensioners. Therefore, the courts believe that a pension covers all the basic needs of a person: the living wage takes into account the food basket, the cost of utility bills, and the required amount of clothing.

For example, if he receives a pension, the court may consider that the father is provided for anyway. The regions automatically raise the pension to the subsistence level for pensioners. Therefore, the courts believe that a pension covers all the basic needs of a person: the living wage takes into account the food basket, the cost of utility bills, and the required amount of clothing.

For example, a pensioner from the Saratov region asked the court to recover alimony from his eldest son, because the man spent his entire pension on medicines, housing and communal services and alimony for minor children.

The court refused the pensioner: the balance of the pension after the payment of alimony and utilities was above the subsistence level in the region. So, a man should have enough money. In addition, he avoided raising his son in childhood - this is what the pensioner's son and his mother said.

paras. 8, 13 Resolutions of the Plenum of the Supreme Court of the Russian Federation dated December 26, 2017 No. 56

56

It is also believed that we have free medicine and, if necessary, a person can be treated in a hospital with drugs at the expense of the budget. That is, if your father does not need expensive life-sustaining drugs that the state does not provide for free, then the risk that he will be able to receive alimony from you is sharply reduced.

For example, a mother from the Chuvash Republic asked to collect alimony from one of her two sons. She also said that she spends her entire pension on medicines and utility bills.

The court refused the woman: she did not prove that she was buying all the expensive medicines prescribed by the surgeon and that she had paid the checks for medicines and food herself. In addition, the plaintiff lived in her sons' house, so she voluntarily bore the costs of housing and communal services. In this case, the court also first of all found that the woman's pension is more than the republican subsistence minimum.

So what? 09/22/18

When you don’t have to pay for treatment and where to complain if they demand money

In addition, you definitely won’t be forced to pay your father for treatment in a sanatorium if you yourself live on the minimum wage. For example, the Saratov court did not recover alimony from an adopted daughter whose income is below the minimum wage and the subsistence level, while the pension of a father with a disability is above the subsistence level.

For example, the Saratov court did not recover alimony from an adopted daughter whose income is below the minimum wage and the subsistence level, while the pension of a father with a disability is above the subsistence level.

The court must also take into account whether you support other people and whether you have any financial obligations. For example, if you have minor children, loans or writ of execution in favor of other claimants, then all this will also protect you from the claims of your father. In total, more than half of the income cannot be recovered from you, and it may be that half of the income is simply not enough for alimony to the father and other obligations.

A father from the Samara region asked to recover alimony from his son in the amount of 5000 R per month, and the son agreed. But during the trial, the court found out that the son has five minor children, and after collecting alimony in favor of his father, he plans to demand in court to reduce the alimony in favor of two children.

The court exacted a symbolic amount in favor of the father - 1000 R per month: it is impossible to infringe on the interests of children.

Art. 99 of the Law "On Enforcement Proceedings"

The risk of becoming indebted to the father is even less if you have brothers or sisters. The court has the right to divide the amount of material assistance necessary for the father among all his children.

For example, a mother from the Moscow region asked to collect alimony from each of her two sons, because she is a person with a disability, had an operation and had to buy expensive medicines. The court exacted 3,000 R alimony from the children. If the child was alone, the amount of alimony from him could be more.

clause 39 of the Resolution of the Plenum of the Supreme Court of the Russian Federation dated December 26, 2017 No. 56

If your father was previously deprived of parental rights, he will not be able to collect alimony from you. But even if once your mother simply went to court with a lawsuit to deprive your father of parental rights, demanded alimony from him, but he did not pay, then the judge can also refuse to give your father alimony. Or he may not refuse if he does not believe that your father shied away from your upbringing.

Or he may not refuse if he does not believe that your father shied away from your upbringing.

For example, in the Tula region, a father with a disability asked to recover alimony from each of his sons in the amount of the minimum wage. But their mother testified in court and said that their father abused alcohol and did not help raise children. To confirm the words of the mother, the sons also submitted a certificate stating that the father has been registered in the drug dispensary for many years.

As a result, the court did not recover maintenance from the children in favor of the retired father. The court also took into account that the father receives a pension, disability payment and monetary compensation for housing and communal services, which in total is more than the subsistence minimum for pensioners in the region.

/list/alimenty-dlya-vseh/

From whom you can and cannot demand alimony

In what order can you be involved in the maintenance of the father

The good news is that you will not find out about the collection of alimony from you in favor of the father after the fact.

Child support in favor of parents is collected in a fixed sum of money, therefore, such a claim cannot be considered by order - when the court, upon application and without summoning the parties, issues an order for collection. This is how alimony is most often collected from parents in favor of children.

clause 3 of Resolution of the Plenum of the Armed Forces of the Russian Federation dated December 26, 2017 No. 56

So it is unlikely that the proceedings will take place without your participation.

From the lawsuit you will find out what the father refers to in his claims and you will be able to give your arguments in response. For example, refer to a small salary, raising children alone, a large debt burden that does not allow helping a father. Arguments can be presented at the court session or written objections. Or even send a representative instead.

Art. 35 Code of Civil Procedure of the Russian Federation

If the father was once deprived of parental rights or he was constantly a debtor for alimony, you can bring a certificate from the bailiffs or a copy of the court decision. The courts also take into account the testimony of the second parent that the parent who applied for alimony did not participate in the life of the child.

The courts also take into account the testimony of the second parent that the parent who applied for alimony did not participate in the life of the child.

Certificates from a neuropsychiatric or narcological dispensary that your parent was registered there in the years when you were growing up will also come in handy.

/spravka/

How to get a certificate from PND

But the fact that you do not want to take care of your father because he did not take care of you is still not the most important thing for the court. What is more important is what kind of pension your father has and what income you have. Therefore, build your objections precisely on numbers.

The court determines the amount of alimony not for life

If the financial or marital status of a parent or child changes, one of them can go to court and demand a change in the amount of alimony - increase or decrease - and also completely cancel the court decision on which this alimony is collected. For a good reason, the court may even write off the alimony debt.

For a good reason, the court may even write off the alimony debt.

Art. 114, 119 SK RF

That is, if the father has already collected alimony from you, then you can arm yourself with court decisions, for example, on collecting money from you in favor of children, mother, bank, public utilities, and ask the court to reduce the amount of alimony in favor of the father .

What is the result

If your father is not deprived of parental rights, you must help him. But not to the detriment of oneself and not to the equivalent of the cost of a car or an apartment. You need to arm yourself with evidence that you cannot or should not help your father. Then the court will confirm: they shouldn't. Or they should, but at 500 R per month.

If you have a question about personal finances, expensive purchases or a family budget, write to us. We will answer the most interesting questions in the magazine.

Ask a question

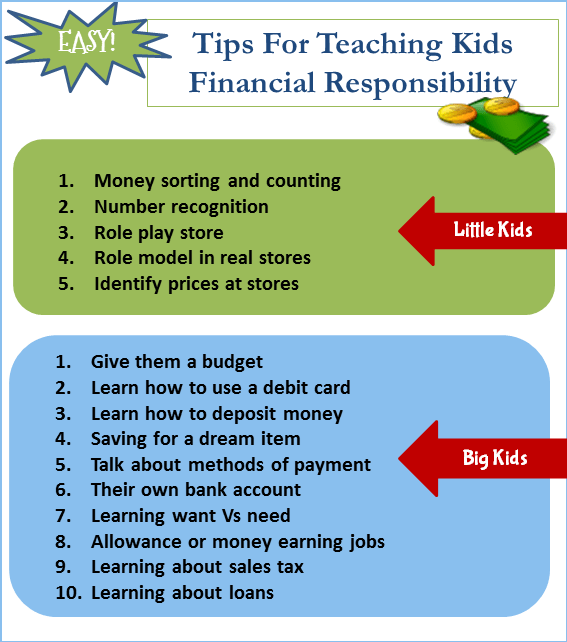

5 rules for financial education of children (and parents)

About half of Russians admit that they do not understand anything about finance.

Many sign documents almost without looking, and one in ten cannot say how much they spend per month. What can we say about educating financial literacy in a child if we ourselves do not know how to handle money. We have put together a few key rules that will help you and your children deal with finances.

Many sign documents almost without looking, and one in ten cannot say how much they spend per month. What can we say about educating financial literacy in a child if we ourselves do not know how to handle money. We have put together a few key rules that will help you and your children deal with finances. Often parents, when discussing financial matters with their children, swim in them themselves. Many of today's mothers and fathers grew up in the Soviet Union, where money was treated as something unworthy of attention, and well-paid people were suspected of being unclean. At 19In the 90s, everything changed dramatically: money began to be considered a measure of success and an assessment of the merits of their owner.

Only now Russians have begun to come to an understanding that money, although important, is still a tool with which you can achieve what you want, but the goals themselves, as well as the ways to achieve them, depend primarily on the nature and priorities of the person himself. Parents, among other things, need to instill in their child the basics of financial literacy, both through exercises and by personal example. But for this you need to remember a few simple rules yourself.

Parents, among other things, need to instill in their child the basics of financial literacy, both through exercises and by personal example. But for this you need to remember a few simple rules yourself.

Rule No. 1. Money does not forgive carelessness

This may seem mystical, because most people believe that money is just colorful pieces of paper or coins of different sizes, in extreme cases, numbers on a bank account: how can they “forgive” or “punish”? But the truth becomes clear if we remember that money is a product of social relations, that is, relations between people in the final analysis. This means that everything related to the financial sector, to one degree or another, obeys the laws of psychology.

Therefore, for example, there is nothing surprising in the fact that a slut can have a mess and chaos in everything - from work to personal life. And a disciplined and systematic person is more likely to have order in other matters, albeit not without some difficulties. And just as most parents teach their children to take care of themselves, put away toys, stick to a schedule, you need to teach them about order and money matters.

And just as most parents teach their children to take care of themselves, put away toys, stick to a schedule, you need to teach them about order and money matters.

At what age should children be introduced to money? Experts say, from three to four years.

First, in the form of a game in the store and the first acquaintance with cash, a story about how different banknotes and coins are similar and different. Then it is worth involving the child in your financial life - in family purchases, discussions of budgets, plans, and so on.

It is important to set a good example. So that children can see from the very beginning: parents treat money thoughtfully and carefully, make purchases rationally and regularly save a part of what they earn. They will see that with such an attitude, money is usually enough for the necessary, and savings allow you to make large purchases, travel, and have fun without harming the family.

Rule #2: Money is not the solution to all problems

Do not overestimate the importance of money. In the end, it is obvious that the most important things in life - respect, love and friendship - cannot be bought for them. Therefore, it is better to make it clear to the child from the very beginning that the world does not revolve around money. There are many other important, interesting and worthy things in it.

In the end, it is obvious that the most important things in life - respect, love and friendship - cannot be bought for them. Therefore, it is better to make it clear to the child from the very beginning that the world does not revolve around money. There are many other important, interesting and worthy things in it.

To do this, of course, parents will have to carefully look at themselves. Doesn't the question become “Where to get money for life?” constant in family conversations? Isn’t it too often in response to a child’s request for a purchase that an annoyed “There is no money for this!” Sounds. Does it happen that a real holiday happens on payday with joyful emotions, plentiful purchases and delicious treats, and a few days before that, family members yearn in anticipation of an advance? After all, all this just leads children to the idea that only money can get rid of problems and give joy.

Also, don't judge your child's friends by the wealth of their families. Otherwise, he will think that a person can be measured by money.

Otherwise, he will think that a person can be measured by money.

Don't tell your child that "Money is everything". Rather, they help in solving many issues or achieving goals, but the main thing still depends on the person himself, his character and actions.

Best

Talk about love, respect, and real human values. The fact that attention to a loved one will not replace an expensive gift. But also about the fact that healthy, harmonious relationships do not exclude the financial component to make them brighter, better and stronger.

Rule #3: Talk about money openly, make decisions together

Often, even among financially educated parents there are those who do not tell their children about money and protect them from discussing the financial issues of the family. Like, “it’s too early”, “we don’t want to spoil it”. However, this is a big mistake, because without a dialogue with the parent, the child will not be able to correctly understand where the money comes from, how and what they spend it on.

On the contrary, it makes sense even for small children to tell in general terms about who earns money in the family, what work is, what adults do there. If a mother is sitting at home on maternity leave, you can tell that this is a worthy occupation - taking care of raising children. Get a real conversation about what's going on in the family.

Discuss money with the whole family - it happens that it turns into mutual education. Children sometimes know better how to use various online services and applications, and grandparents have more life experience - they can give practical advice on optimizing the budget. So you can not only increase the level of financial literacy, but also further unite the family.

And, of course, it is desirable to talk not only about income, but also to jointly plan expenses, discuss the budget, compare savings or investment opportunities. All this taken together is the foundation of competent financial behavior. And the child can learn about various banking products, loans, deposits later.

How impossible

When you discuss upcoming purchases, don't say "No money." The child may take this phrase as a signal that "there is no way out" or even as a synonym for disaster. This will cause unnecessary stress.

Best

Even if the family has temporary financial difficulties, the child deserves clear explanations why you need to wait with the desired purchase. In addition, depending on age, you can offer different options for how to save up or earn money for what you want.

Rule #4: Give children money for personal expenses

According to statistics, most often children receive their first money in adolescence. However, according to psychologists, already before elementary school, the child is ready to make small independent purchases. This may have a positive effect on his attitude towards money in the future.

Another mistake that many parents make is to give money randomly, for academic success or household chores. But "paying" for everything that, by definition, is the responsibility of children as family members, reduces their motivation. And if you give money irregularly and unsystematically, then the child will not learn how to plan and distribute finances. All this reduces the educational effect of the issuance of pocket money to zero.

But "paying" for everything that, by definition, is the responsibility of children as family members, reduces their motivation. And if you give money irregularly and unsystematically, then the child will not learn how to plan and distribute finances. All this reduces the educational effect of the issuance of pocket money to zero.

How impossible

Do not enter "rates" for good grades or washed dishes. By doing this, you will only spoil your relationship and reduce the motivation for knowledge. It is also wrong to give children "bonuses" just like that - from a good mood or after receiving an annual bonus. It is better to immediately come up with and discuss with the child when he receives money, and adhere to these rules in any circumstances.

Best

Give your child a reasonable amount of income once a week or two. The amount and frequency of payments should be discussed in advance, balancing his interests and needs and his capabilities. You can come up with a system of rewards, but not for household chores or school success, but for something that is not included in children's duties. It also makes sense to discuss with the child at the end of the week or month (but only with his consent, of course), what he had enough pocket money for, and what he didn’t have, and what needs to be done so that there is enough money.

You can come up with a system of rewards, but not for household chores or school success, but for something that is not included in children's duties. It also makes sense to discuss with the child at the end of the week or month (but only with his consent, of course), what he had enough pocket money for, and what he didn’t have, and what needs to be done so that there is enough money.

How much money to give a child?

There are a number of cases when a "bonus" to a child will become both a positive lesson and motivation for him. For example, if he helped you choose a product in an online store and saved the family money. Some of the difference may go into his pocket. Or if he helped you in your work. Many children are now great at making presentations, for example. If you involve a child in your work, he will better understand what you are doing, and once again make sure that money is paid for a reason.

Rule #5: Trust children

Some parents try to protect their children from financial mistakes. For example, they are afraid to let them go to the store alone. Often parents insist that their child's pocket money be "in plain sight" - for fear that he may spend it irrationally or even lose it. In essence, children are not in control of their own - as they are told - money.

For example, they are afraid to let them go to the store alone. Often parents insist that their child's pocket money be "in plain sight" - for fear that he may spend it irrationally or even lose it. In essence, children are not in control of their own - as they are told - money.

The result is a reduction in responsibility in the distribution of money and the formation of incorrect behavior strategies. Children either learn to hide money from their parents, or tend to spend it as soon as possible so as not to lose it due to some unexpected decision of their father or mother. The first is harmful to intra-family relations, the second is harmful to the financial future of the child. It turns out that in order to form the right attitude of children to money, parents need to start with themselves - learn to trust the child.

What can be done. Practical tasks, attempts to save up for a goal or be responsible for one's own item in the family budget well bring up responsibility and the ability to plan in a child. For example, you can instruct him to ensure that there is always bread and milk at home. At the same time, it’s not scary if you stay a couple of times in the morning without an omelette or a sandwich - but this will become an object lesson for the child.

For example, you can instruct him to ensure that there is always bread and milk at home. At the same time, it’s not scary if you stay a couple of times in the morning without an omelette or a sandwich - but this will become an object lesson for the child.

Even buying a pet can help develop financial literacy. For example, you can arrange for the child to estimate the weekly budget for his maintenance and pay for food at his own expense. The main condition is that only he is responsible for the food for the pet, which he himself must buy in a nearby store. This will teach not only responsibility, but also care.

Although the Central Bank, the Ministry of Finance, schools and banks do a lot to teach children the basics of financial literacy, the child receives its first lessons in the family. Even if the parents don't think about it. In any case, their attitude to money, good or bad habits in this area significantly affect the future financial behavior of the child. On the model of life that he chooses for himself in the future.

On the model of life that he chooses for himself in the future.

The best thing that parents can do is to set a personal example for their children in a correct, effective and responsible relationship with money.

So, if you want to raise a child financially successful or at least just independent, start with yourself. From the introduction into your life of the rules and principles that we described above.

This material is part of a large project dedicated to the development of children's personal potential and key competencies of the 21st century. What is the project about? We talk about the child and his development as a person, not an object of the educational process. We explain how the world is changing and show what skills will help a child live harmoniously in a changing reality. Other materials of the project cover the topics of development of social-emotional intelligence, financial and digital literacy, cognitive development, inclusion in school, etc.