Feeling depressed about money

Coping with Financial Stress - HelpGuide.org

stress

Feeling overwhelmed by money worries? Whatever your circumstances, there are ways to get through these tough economic times, ease stress and anxiety, and regain control of your finances.

Understanding financial stress

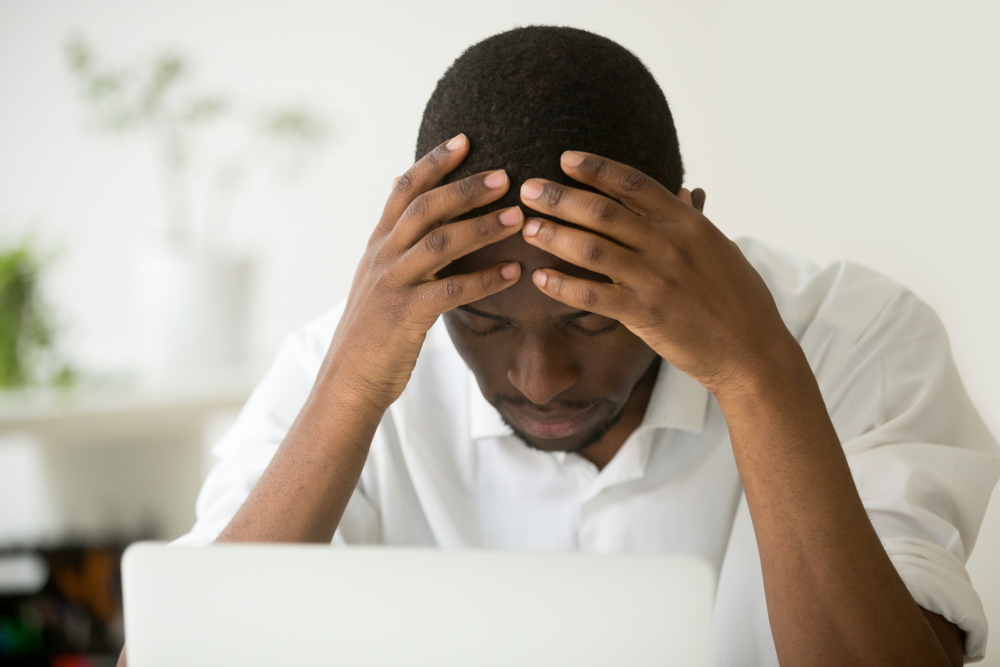

If you’re worried about money, you’re not alone. Many of us, from all over the world and from all walks of life, are having to deal with financial stress and uncertainty at this difficult time. Whether your problems stem from a loss of work, escalating debt, unexpected expenses, or a combination of factors, financial worry is one of the most common stressors in modern life. Even before the global coronavirus pandemic and resulting economic fallout, an American Psychological Association (APA) study found that 72% of Americans feel stressed about money at least some of the time. The recent economic difficulties mean that even more of us are now facing financial struggles and hardship.

Like any source of overwhelming stress, financial problems can take a huge toll on your mental and physical health, your relationships, and your overall quality of life. Feeling beaten down by money worries can adversely impact your sleep, self-esteem, and energy levels. It can leave you feeling angry, ashamed, or fearful, fuel tension and arguments with those closest to you, exacerbate pain and mood swings, and even increase your risk of depression and anxiety. You may resort to unhealthy coping mechanisms, such as drinking, abusing drugs, or gambling to try to escape your worries. In the worst circumstances, financial stress can even prompt suicidal thoughts or actions. But no matter how hopeless your situation seems, there is help available. By tackling your money problems head on, you can find a way through the financial quagmire, ease your stress levels, and regain control of your finances—and your life.

Effects of financial stress on your health

While we all know deep down there are many more important things in life than money, when you’re struggling financially fear and stress can take over your world. It can damage your self-esteem, make you feel flawed, and fill you with a sense of despair. When financial stress becomes overwhelming, your mind, body, and social life can pay a heavy price.

When financial stress becomes overwhelming, your mind, body, and social life can pay a heavy price.

[Read: Stress Symptoms, Signs, and Causes]

Financial stress can lead to:

Insomnia or other sleep difficulties. Nothing will keep you tossing and turning at night more than worrying about unpaid bills or a loss of income.

Weight gain (or loss). Stress can disrupt your appetite, causing you to anxiously overeat or skip meals to save money.

Depression. Living under the cloud of money problems can leave anyone feeling down, hopeless, and struggling to concentrate or make decisions. According to a study at the University of Nottingham in the UK, people who struggle with debt are more than twice as likely to suffer from depression.

Anxiety. Money can be a safety net; without it, you may feel vulnerable and anxious. And all the worrying about unpaid bills or loss of income can trigger anxiety symptoms such as a pounding heartbeat, sweating, shaking, or even panic attacks.

Relationship difficulties. Money is often cited as the most common issue couples argue about. Left unchecked, financial stress can make you angry and irritable, cause a loss of interest in sex, and wear away at the foundations of even the strongest relationships.

Social withdrawal. Financial worries can clip your wings and cause you to withdraw from friends, curtail your social life, and retreat into your shell—which will only make your stress worse.

Physical ailments such as headaches, gastrointestinal problems, diabetes, high blood pressure, and heart disease. In countries without free healthcare, money worries may also cause you to delay or skip seeing a doctor for fear of incurring additional expenses.

Unhealthy coping methods, such as drinking too much, abusing prescription or illegal drugs, gambling, or overeating. Money worries can even lead to self-harm or thoughts of suicide.

If you are feeling suicidal…

Your money problems may seem overwhelming and permanent right now. But with time, things will get better and your outlook will change, especially if you get help. There are many people who want to support you during this difficult time, so please reach out!

But with time, things will get better and your outlook will change, especially if you get help. There are many people who want to support you during this difficult time, so please reach out!

Read Are You Feeling Suicidal?, call 1-800-273-TALK in the U.S., or find a helpline in your country at IASP or Suicide.org.

The vicious cycle of poor financial health and poor mental health

A number of studies have demonstrated a cyclical link between financial worries and mental health problems such as depression, anxiety, and substance abuse.

Financial problems adversely impact your mental health. The stress of debt or other financial issues leaves you feeling depressed or anxious.

The decline in your mental health makes it harder to manage money. You may find it harder to concentrate or lack the energy to tackle a mounting pile of bills. Or you may lose income by taking time off work due to anxiety or depression.

These difficulties managing money lead to more financial problems and worsening mental health problems, and so on. You become trapped in a downward spiral of increasing money problems and declining mental health.

No matter how bleak your situation may seem at the moment, there is a way out. These strategies can help you to break the cycle, ease the stress of money problems, and find stability again.

Dealing with financial stress tip 1: Talk to someone

When you’re facing money problems, there’s often a strong temptation to bottle everything up and try to go it alone. Many of us even consider money a taboo subject, one not to be discussed with others. You may feel awkward about disclosing the amount you earn or spend, feel shame about any financial mistakes you’ve made, or embarrassed about not being able to provide for your family. But bottling things up will only make your financial stress worse. In the current economy, where many people are struggling through no fault of their own, you’ll likely find others are far more understanding of your problems.

[Read: Social Support for Stress Relief]

Not only is talking face-to-face with a trusted friend or loved one a proven means of stress relief, but speaking openly about your financial problems can also help you put things in perspective. Keeping money worries to yourself only amplifies them until they seem insurmountable. The simple act of expressing your problems to someone you trust can make them seem far less intimidating.

- The person you talk to doesn’t have to be able to fix your problems or offer financial help.

- To ease your burden, they just need to be willing to talk things out without judging or criticizing.

- Be honest about what you’re going through and the emotions you’re experiencing.

- Talking over your worries can help you make sense of what you’re facing and your friend or loved one may even be able to come up with solutions that you hadn’t thought of alone.

Getting professional advice

Depending on where you live, there are a number of organizations that offer free counseling on dealing with financial problems, whether it’s managing debt, creating and sticking to a budget, finding work, communicating with creditors, or claiming benefits or financial assistance. (See the “Get more help” section below for links).

(See the “Get more help” section below for links).

Whether or not you have a friend or loved one to talk to for emotional support, getting practical advice from an expert is always a good idea. Reaching out is not a sign of weakness and it doesn’t mean that you’ve somehow failed as a provider, parent, or spouse. It just means that you’re wise enough to recognize your financial situation is causing you stress and needs addressing.

With over 25,000 licensed counselors, BetterHelp has a therapist that fits your needs. It's easy, affordable, and convenient.

GET 20% OFF

Online-Therapy.com is a complete toolbox of support, when you need it, on your schedule. It only takes a few minutes to sign up.

GET 20% OFF

Teen Counseling is an online therapy service for teens and young adults. Connect with your counselor by video, phone, or chat.

GET 20% OFF

Opening up to your family

Financial problems tend to impact the whole family and enlisting your loved ones’ support can be crucial in turning things around. Even if you take pride in being self-sufficient, keep your family up to date on your financial situation and how they can help you save money.

Even if you take pride in being self-sufficient, keep your family up to date on your financial situation and how they can help you save money.

Let them express their concerns. Your loved ones are probably worried—about both you and the financial stability of your family unit. Listen to their concerns and allow them to offer suggestions on how to resolve the financial problems you’re facing.

Make time for (inexpensive) family fun. Set aside regular time where you can enjoy each other’s company, let off steam, and forget about your financial worries. Walking in the park, playing games, or exercising together doesn’t have to cost money but it can help ease stress and keep the whole family positive.

Tip 2: Take inventory of your finances

If you’re struggling to make ends meet, you may think you can ease your stress by leaving bills unopened, avoiding phone calls from creditors, or ignoring bank and credit card statements. But denying the reality of your situation will only make things worse in the long run. The first step to devising a plan to solve your money problems is to detail your income, debt, and spending over the course of at least one month.

The first step to devising a plan to solve your money problems is to detail your income, debt, and spending over the course of at least one month.

A number of websites and smartphone apps can help you keep track of your finances moving forward or you can work backwards by gathering receipts and examining bank and credit card statements. Obviously, some money difficulties are easier to solve than others, but by taking inventory of your finances you’ll have a much clearer idea of where you stand. And as daunting or painful as the process may seem, tracking your finances in detail can also help you start to regain a much-needed sense of control over your situation.

Include every source of income. In addition to any salary, include bonuses, benefits, alimony, child support, or any interest you receive.

Keep track of ALL your spending. When you’re faced with a pile of past-due bills and mounting debt, buying a coffee on the way to work may seem like an irrelevant expense. But seemingly small expenses can mount up over time, so keep track of everything. Understanding exactly how you spend your money is key to budgeting and devising a plan to address your financial problems.

But seemingly small expenses can mount up over time, so keep track of everything. Understanding exactly how you spend your money is key to budgeting and devising a plan to address your financial problems.

List your debts. Include past-due bills, late fees, and list minimum payments due as well as any money you owe to family or friends.

Identify spending patterns and triggers. Does boredom or a stressful day at work cause you to head to the mall or start online shopping? When the kids are acting out, do you keep them quiet with expensive restaurant or takeout meals, rather than cooking at home? Once you’re aware of your triggers you can find healthier ways of coping with them than resorting to “retail therapy”.

Look to make small changes. Spending money on things like a morning newspaper, lunchtime sandwich, or break-time cigarettes can add up to a significant monthly outlay. While it may be unreasonable to deny yourself every small pleasure, cutting down on nonessential spending and finding small ways to reduce your daily expenditure can really help to free up extra cash to pay off bills.

Eliminate impulse spending. Ever seen something online or in a shop window that you just had to buy? Impulsive buying can wreck your budget and max out your credit cards. To break the habit, try making a rule that you’ll wait a week before making any new purchase.

Go easy on yourself. As you review your debt and spending habits, remember that anyone can get into financial difficulties, especially at times like this. Don’t use this as an excuse to punish yourself for any perceived financial mistakes. Give yourself a break and focus on the aspects you can control as you look to move forward.

When your financial problems go beyond money

Sometimes, the causes for your financial difficulties may lie elsewhere. For example, money troubles can stem from problem gambling, fraud abuse, or a mental health issue, such as overspending during a bipolar manic episode.

To prevent the same financial problems recurring, it’s imperative you address both the underlying issue and the money troubles it’s created in your life.

Tip 3: Make a plan—and stick to it

Just as financial stress can be caused by a wide range of different money problems, so there are an equally wide range of possible solutions. The plan to address your specific problem could be to live within a tighter budget, lower the interest rate on your credit card debt, curb your online spending, seek government benefits, declare bankruptcy, or to find a new job or additional source of income.

If you’ve taken inventory of your financial situation, eliminated discretionary and impulse spending, and your outgoings still exceed your income, there are essentially three choices open to you: increase your income, lower your spending, or both. How you go about achieving any of those goals will require making a plan and following through on it.

- Identify your financial problem. Having taken inventory, you should be able to clearly identify the financial problem you’re facing. It may be that you have too much credit card debt, not enough income, or you overspend on unnecessary purchases when you feel stressed or anxious.

Or perhaps, it’s a combination of problems. Make a separate plan for each one.

Or perhaps, it’s a combination of problems. Make a separate plan for each one. - Devise a solution. Brainstorm ideas with your family or a trusted friend, or consult a free financial counseling service. You may decide that talking to credit card companies and requesting a lower interest rate would help solve your problem. Or maybe you need to restructure your debt, eliminate your car payment, downsize your home, or talk to your boss about working overtime.

- Put your plan into action. Be specific about how you can follow through on the solutions you’ve devised. Perhaps that means cutting up credit cards, networking for a new job, registering at a local food bank, or selling things on eBay to pay off bills, for example.

- Monitor your progress. As we’ve all experienced recently, events that impact your financial health can happen quickly, so it’s important to regularly review your plan. Are some aspects working better than others? Do changes in interest rates, your monthly expenses, or your hourly wage, for example, mean you should revise your plan?

- Don’t get derailed by setbacks.

We’re all human and no matter how tight your plan, you may stray from your goal or something unexpected could happen to derail you. Don’t beat yourself up, but get back on track as soon as possible.

We’re all human and no matter how tight your plan, you may stray from your goal or something unexpected could happen to derail you. Don’t beat yourself up, but get back on track as soon as possible.

The more detailed you can make your plan, the less powerless you’ll feel over your financial situation.

Tip 4: Create a monthly budget

Whatever your plan to relieve your financial problems, setting and following a monthly budget can help keep you on track and regain your sense of control.

- Include everyday expenses in your budget, such as groceries and the cost of traveling to work, as well as monthly rent, mortgage, and utility bills.

- For items that you pay annually, such as car insurance or property tax, divide them by 12 so you can set aside money each month.

- If possible, try to factor in unexpected expenses, such as a medical co-pay or prescription charge if you fall sick, or the cost of home or car repairs.

- Set up automatic payments wherever possible to help ensure bills are paid on time and you avoid late payments and interest rate hikes.

- Prioritize your spending. If you’re having trouble covering your expenses each month, it can help to prioritize where your money goes first. For example, feeding and housing yourself and your family and keeping the power on are necessities. Paying your credit card isn’t—even if you’re behind on your payments and have debt collection companies harassing you.

- Keep looking for ways to save money. Most of us can find something in our budget that we can eliminate to help make ends meet. Regularly review your budget and look for ways to trim expenses.

- Enlist support from your spouse, partner, or kids. Make sure everyone in your household is pulling in the same direction and understands the financial goals you’re working towards.

Tip 5: Manage your overall stress

Resolving financial problems tends to involve small steps that reap rewards over time. In the current economic climate, it’s unlikely your financial difficulties will disappear overnight. But that doesn’t mean you can’t take steps right away to ease your stress levels and find the energy and peace of mind to better deal with challenges in the long-term.

[Read: Stress Management]

Get moving. Even a little regular exercise can help ease stress, boost your mood and energy, and improve your self-esteem. Aim for 30 minutes on most days, broken up into short 10-minute bursts if that’s easier.

Practice a relaxation technique. Take time to relax each day and give your mind a break from the constant worrying. Meditating, breathing exercises, or other relaxation techniques are excellent ways to relieve stress and restore some balance to your life.

Don’t skimp on sleep. Feeling tired will only increase your stress and negative thought patterns. Finding ways to improve your sleep during this difficult time will help both your mind and body.

Boost your self-esteem. Rightly or wrongly, experiencing financial problems can cause you to feel like a failure and impact your self-esteem. But there are plenty of other, more rewarding ways to improve your sense of self-worth. Even when you’re struggling yourself, helping others by volunteering can increase your confidence and ease stress, anger, and anxiety—not to mention aid a worthy cause. Or you could spend time in nature, learn a new skill, or enjoy the company of people who appreciate you for who you are, rather than for your bank balance.

Even when you’re struggling yourself, helping others by volunteering can increase your confidence and ease stress, anger, and anxiety—not to mention aid a worthy cause. Or you could spend time in nature, learn a new skill, or enjoy the company of people who appreciate you for who you are, rather than for your bank balance.

Eat healthy food. A healthy diet rich in fruit, vegetables, and omega-3s can help support your mood and improve your energy and outlook. And you don’t have to spend a fortune; there are ways to eat well on a budget.

Be grateful for the good things in your life. When you’re plagued by money worries and financial uncertainty, it’s easy to focus all your attention on the negatives. While you don’t have to ignore reality and pretend everything’s fine, you can take a moment to appreciate a close relationship, the beauty of a sunset, or the love of a pet, for example. It can give your mind a break from the constant worrying, help boost your mood, and ease your stress.

Authors: Lawrence Robinson and Melinda Smith, M.A.

- References

Trauma- and Stressor-Related Disorders. (2013). In Diagnostic and Statistical Manual of Mental Disorders. American Psychiatric Association. https://doi.org/10.1176/appi.books.9780890425787.x07_Trauma_and_Stressor_Related_Disorders

Inc, Gallup. “The U.S. Healthcare Cost Crisis.” Gallup.com. Accessed November 16, 2021. https://news.gallup.com/poll/248081/westhealth-gallup-us-healthcare-cost-crisis.aspx

Anderson, Norman B, Cynthia D Belar, Steven J Breckler, Katherine C Nordal, David W Ballard, Lynn F Bufka, Luana Bossolo, Sophie Bethune, Angel Brownawell, and Katelynn Wiggins. Stress in America: Paying with our Health. “AMERICAN PSYCHOLOGICAL ASSOCIATION,” n.

d., 23. https://www.apa.org/news/press/releases/stress/2014/stress-report.pdf

d., 23. https://www.apa.org/news/press/releases/stress/2014/stress-report.pdfRamsey Solutions. “Money, Marriage, and Communication.” Accessed November 16, 2021. https://www.ramseysolutions.com/relationships/money-marriage-communication-research

“At What Costs? Student Loan Debt, Debt Stress, and Racially/Ethnically Diverse College Students’ Perceived Health. – PsycNET.” Accessed November 16, 2021. https://doi.apa.org/doiLanding?doi=10.1037%2Fcdp0000207

Richardson, Thomas, Peter Elliott, and Ronald Roberts. “The Relationship between Personal Unsecured Debt and Mental and Physical Health: A Systematic Review and Meta-Analysis.” Clinical Psychology Review 33, no. 8 (December 1, 2013): 1148–62. https://doi.org/10.1016/j.cpr.2013.08.009

Warth, Jacqueline, Marie-Therese Puth, Judith Tillmann, Johannes Porz, Ulrike Zier, Klaus Weckbecker, and Eva Münster. “Over-Indebtedness and Its Association with Sleep and Sleep Medication Use.” BMC Public Health 19, no.

1 (July 17, 2019): 957. https://doi.org/10.1186/s12889-019-7231-1

1 (July 17, 2019): 957. https://doi.org/10.1186/s12889-019-7231-1Saleh, Dalia, Nathalie Camart, Fouad Sbeira, and Lucia Romo. “Can We Learn to Manage Stress? A Randomized Controlled Trial Carried out on University Students.” PLOS ONE 13, no. 9 (September 5, 2018): e0200997. https://doi.org/10.1371/journal.pone.0200997

“Stress, Social Support, and the Buffering Hypothesis. – PsycNET.” Accessed November 15, 2021. https://doi.apa.org/doiLanding?doi=10.1037%2F0033-2909.98.2.310

Salmon, P. “Effects of Physical Exercise on Anxiety, Depression, and Sensitivity to Stress: A Unifying Theory.” Clinical Psychology Review 21, no. 1 (February 2001): 33–61. https://doi.org/10.1016/s0272-7358(99)00032-x

Toussaint, Loren, Quang Anh Nguyen, Claire Roettger, Kiara Dixon, Martin Offenbächer, Niko Kohls, Jameson Hirsch, and Fuschia Sirois. “Effectiveness of Progressive Muscle Relaxation, Deep Breathing, and Guided Imagery in Promoting Psychological and Physiological States of Relaxation.

” Evidence-Based Complementary and Alternative Medicine 2021 (July 3, 2021): e5924040. https://doi.org/10.1155/2021/5924040

” Evidence-Based Complementary and Alternative Medicine 2021 (July 3, 2021): e5924040. https://doi.org/10.1155/2021/5924040

Managing Job Loss and Financial Stress (PDF) – Helping yourself and your family cope with stress and financial worries following job loss. (University of Hawaii)

Managing Debt – Steps you can take to deal with debt. (Federal Trade Commission)

Managing money and budgeting – Tips for creating a family budget. (raisingchildren.net.au)

Make a Budget (PDF) – Simple worksheet to help you create a budget. (Federal Trade Commission)

Money Stress Weighing on Americans’ Health (PDF) – Details of the 2015 Stress in America: Paying with Our Health survey from the American Psychological Association. (APA)

Find financial resources

- In the U.S.: Find U.S. Government Services and Information including Dealing with Debt, Unemployment Help, and Getting Help with Living Expenses. Or call 1-844-872-4681.

(USA gov)

(USA gov) - UK: Get help with debt and housing problems from Citizens Advice, contact a free debt service at National Debtline or Stepchange, or seek free financial advice from the government’s Money Advice Service.

- Australia: Find Government Services, get free Financial Counselling or call the National Debt Helpline at 1800 007 007.

- Canada: Find government services and information for Managing Debt and Benefits.

- India: Find advice and help with government schemes from Citizens Advice Bureau.

Last updated: December 5, 2022

SAMHSA’s National Helpline | SAMHSA

Your browser is not supported

Switch to Chrome, Edge, Firefox or Safari

Main page content

-

SAMHSA’s National Helpline is a free, confidential, 24/7, 365-day-a-year treatment referral and information service (in English and Spanish) for individuals and families facing mental and/or substance use disorders.

Also visit the online treatment locator.

SAMHSA’s National Helpline, 1-800-662-HELP (4357) (also known as the Treatment Referral Routing Service), or TTY: 1-800-487-4889 is a confidential, free, 24-hour-a-day, 365-day-a-year, information service, in English and Spanish, for individuals and family members facing mental and/or substance use disorders. This service provides referrals to local treatment facilities, support groups, and community-based organizations.

Also visit the online treatment locator, or send your zip code via text message: 435748 (HELP4U) to find help near you. Read more about the HELP4U text messaging service.

The service is open 24/7, 365 days a year.

English and Spanish are available if you select the option to speak with a national representative. Currently, the 435748 (HELP4U) text messaging service is only available in English.

Currently, the 435748 (HELP4U) text messaging service is only available in English.

In 2020, the Helpline received 833,598 calls. This is a 27 percent increase from 2019, when the Helpline received a total of 656,953 calls for the year.

The referral service is free of charge. If you have no insurance or are underinsured, we will refer you to your state office, which is responsible for state-funded treatment programs. In addition, we can often refer you to facilities that charge on a sliding fee scale or accept Medicare or Medicaid. If you have health insurance, you are encouraged to contact your insurer for a list of participating health care providers and facilities.

The service is confidential. We will not ask you for any personal information. We may ask for your zip code or other pertinent geographic information in order to track calls being routed to other offices or to accurately identify the local resources appropriate to your needs.

No, we do not provide counseling. Trained information specialists answer calls, transfer callers to state services or other appropriate intake centers in their states, and connect them with local assistance and support.

-

Suggested Resources

What Is Substance Abuse Treatment? A Booklet for Families

Created for family members of people with alcohol abuse or drug abuse problems. Answers questions about substance abuse, its symptoms, different types of treatment, and recovery. Addresses concerns of children of parents with substance use/abuse problems.It's Not Your Fault (NACoA) (PDF | 12 KB)

Assures teens with parents who abuse alcohol or drugs that, "It's not your fault!" and that they are not alone. Encourages teens to seek emotional support from other adults, school counselors, and youth support groups such as Alateen, and provides a resource list.After an Attempt: A Guide for Taking Care of Your Family Member After Treatment in the Emergency Department

Aids family members in coping with the aftermath of a relative's suicide attempt. Describes the emergency department treatment process, lists questions to ask about follow-up treatment, and describes how to reduce risk and ensure safety at home.

Describes the emergency department treatment process, lists questions to ask about follow-up treatment, and describes how to reduce risk and ensure safety at home.Family Therapy Can Help: For People in Recovery From Mental Illness or Addiction

Explores the role of family therapy in recovery from mental illness or substance abuse. Explains how family therapy sessions are run and who conducts them, describes a typical session, and provides information on its effectiveness in recovery.For additional resources, please visit the SAMHSA Store.

Last Updated: 08/30/2022

9 life truths that will help you get rid of stress because of money - Ilya Solomennikov on vc.ru

2242 views

Financial problems are the reasons for the constant unrest of most people. Many families only make ends meet, barely reach their salaries, have debts on loans. They are unhappy, they look into the future with a bleak look.

This condition is only partly due to the lack of means of subsistence. Often the reason for the bleak situation of a person or family is a misunderstanding of simple truths about money. Therefore, simply by looking for an additional source of income, the problem of permanent stress due to financial difficulties cannot be solved. It is advisable to slightly or thoroughly change your worldview. nine0003

Of course, by increasing the amount of your income, you will be able to get rid of want for a while and forget about worries for the time being. But the calm will certainly not last long, and gloomy thoughts will return again. You can solve financial problems once and for all only by changing your attitude to money and the material side of life in general. Here are some things you need to learn in order to stop constantly worrying about money:

1. For a happy and comfortable life, a person needs much less than he thinks

Surely you know that many of the inhabitants of the Earth do not have things familiar to us, without which, it would seem, it is impossible to do. For example, various gadgets, household appliances, cars, branded shoes and clothes, beautiful furniture. Business has simply imposed on society the idea that it is impossible to do without such attributes.

For example, various gadgets, household appliances, cars, branded shoes and clothes, beautiful furniture. Business has simply imposed on society the idea that it is impossible to do without such attributes.

People have been taught that the purchase of various goods that are produced by the richest corporations is a natural need. If a person is not able to buy an advertised product, he begins to experience dissatisfaction with his life. To get rid of stress due to low solvency, you should understand and accept that many things can be painlessly dispensed with. nine0003

2. Money does not bring happiness

Not all rich people are completely satisfied with their lives. Many of those who have millions and billions are not at all so happy, joyful. Among them are many individuals who have been suffering from depression for years. Therefore, the statement that it is necessary to have a lot of money to be happy is erroneous. Of course, money gives a feeling of stability and security. But they can't make a person happy. True pleasure is given by other things - love, closeness and health of relatives, peace of mind, hobbies and many other joys available to ordinary people, not necessarily rich. nine0003

But they can't make a person happy. True pleasure is given by other things - love, closeness and health of relatives, peace of mind, hobbies and many other joys available to ordinary people, not necessarily rich. nine0003

3. Money is not the main purpose of activity, professional, creative or otherwise

Financial reward is not always the main motivation. Often a job that is not to their liking does not bring any satisfaction even with a high salary. Of course, earning an income that is commensurate with the effort put in can reduce work-related stress. But it's hard to work just for the money. In addition to material benefits, work should also bring moral satisfaction, promote self-development, the manifestation of talents and abilities. nine0003

4. Rich people also have their problems and difficulties

Of course, the poor have many financial and other problems. But wealthy people also have difficulties, and quite a few. Not everyone thinks about it, believing that wealth is a panacea for all ills. This is not true.

This is not true.

Money has both a light and a dark side, it brings both joy and problems. Wealth, for example, significantly distorts moral principles, makes a person more rigid, cynical and callous, as well as soulless and arrogant. Not everyone who managed to achieve a high position and excellent prosperity remained kind, humane, compassionate. nine0003

Big money often changes people for the worse, which harms them and their loved ones first of all. In addition, there are problems that even money cannot solve. So, they will not help you find true love, true friendship, establish good and sincere relationships with people. On the contrary, all this is rather accessible to people with low incomes. It is more difficult for the rich to find simple human relationships in their environment.

5. The pursuit of wealth deprives a person of the joy of life

The desire to earn more money takes a lot of time, effort and health. The waste of such valuable, sometimes irreplaceable resources contributes to the depreciation of the really important and significant that is in our lives.

It is better to get rid of the obsessive desire to get rich. This will not only reduce stress levels, but also free up resources and time for other, more constructive activities. The things that bring true joy are the enjoyment of natural beauties, the pleasure of watching your child grow up, the opportunity to get enough sleep, to have good health. For a person who is satisfied with life, calm, but not a loafer, financial problems will surely be gradually resolved. nine0003

6. The presence of restrictions is not harmful, but beneficial

There must be boundaries in everything. They form a certain way of life, its basis. Not total, but some limitations motivate a person to seek and find happiness, joy in what he has here and now under real circumstances, and not in fantasies.

In relation to finance, such boundaries will be a plan of expenses for a certain period of time. Those who want to live in peace and without debts cannot do without it. After all, if a person lives beyond their means, their expenses exceed their income, and life gets out of control. nine0003

After all, if a person lives beyond their means, their expenses exceed their income, and life gets out of control. nine0003

Planning a personal budget helps to adjust your needs to the level of available income, not to get into debt. It disciplines, gives confidence in the ability to keep your life under control. A smart person lives within their means, and does not spend more than they earn.

7. Generosity is wonderful

Money should not be regretted if it is spent for good purposes. Generosity makes a person happier. As practice shows, those people who are not afraid to part with money have better health, a more eventful life, and also a much lower level of stress than those who prefer to take care only of profit. Therefore, it is desirable for everyone to engage in charity, regardless of income level. nine0003

8. The feeling of security, which is based on the possession of money, property, is unstable and passes quickly

It is generally believed that only with wealth can one feel confident in the future and protected from all adversity. A very controversial opinion. The accumulation of money and property is not capable of providing security: there are enough examples in history when people lost their assets in a lifetime in one day.

A very controversial opinion. The accumulation of money and property is not capable of providing security: there are enough examples in history when people lost their assets in a lifetime in one day.

To feel secure, a person must be surrounded by the warmth and love of loved ones. Many rich people do not have this due to the fact that the accumulation of money, their multiplication and preservation has become the most important thing in life. Everything else faded into the background. In choosing partners for relationships and families, they are guided by the stereotypes of appearance and behavior imposed by the media. Classical values, including kindness, fidelity, beauty of the soul, sensitivity, without which it is impossible to experience the highest enjoyment of life, are ignored and squeezed out of the set of needs of rich people. nine0003

What kind of internal security, confidence in loved ones can we talk about if they stay close for the sake of money and property? The accumulation of wealth will not bring joy, a sense of security and peace.

9. Money should be taken only as a tool to achieve the goal

With the help of money, a person receives necessary things (food, drink, clothing, a roof over his head) and luxury goods. Money enables people to do what they love. That is, they are only a tool for meeting needs, but by no means an end in itself and not the meaning of life. Being stressed about not being able to get more is not the best option. Stress negatively affects both physical and mental health. nine0003

The accumulation of capital, its saving and multiplication at all times were considered the main causes of anxiety and worries. If you dedicate your life to endlessly solving financial problems, you will provide yourself with a rather dull existence. Smartly balance your needs and real incomes to live peacefully and happily!

Maxim Malyavin on whether to blame the lack of money for all troubles - Gazeta.Ru

“Money will not make you happier,” Arnold Schwarzenegger once voiced the well-known maxim.+0076-0078+(30).jpg) And he immediately brought an iron argument to confirm: "I have 50 million now, and I'm just as happy as when I had 48 million." Iron logic in iron Arnie, what can I say. And how is it really? Too often one hears, both at receptions and at medical examinations, where we, psychiatrists, are invariably present, that poverty is to blame. There was less money - and the depression began. nine0003

And he immediately brought an iron argument to confirm: "I have 50 million now, and I'm just as happy as when I had 48 million." Iron logic in iron Arnie, what can I say. And how is it really? Too often one hears, both at receptions and at medical examinations, where we, psychiatrists, are invariably present, that poverty is to blame. There was less money - and the depression began. nine0003

I will allow myself not only to doubt, but rather to clarify some points linking poverty and depression. Because not everything in this pair is so unambiguous. And not always the first is the cause, and the second is the effect. It just takes a little thought and clarification of a number of points.

The fact is that under depression, the average person, who is not versed in the subtleties of psychiatric terminology, most often means several radically different conditions, which are united by one sign: low mood. And it is not his fault that he puts in one basket both endogenous depression, and reactive depression, and depressive (or rather, more often subdepressive, not up to full-blown clinical depression) syndrome with neurosis, and just a bad mood outside of any illness. And now let's go through each of the listed points and take a closer look, and at the same time we will figure out: how dependent is each of them on material wealth? nine0003

And now let's go through each of the listed points and take a closer look, and at the same time we will figure out: how dependent is each of them on material wealth? nine0003

The first item is endogenous depression.

Either in terms of bipolar affective disorder (or BPD, as it used to be called), or in terms of recurrent depressive episodes.

These episodes are vivid, powerful, with a risk of suicide, with a clearly expressed depressive triad (and this is a sharply lowered mood - one; inhibited thinking - two; and inhibited movements - three), with longing, tearing the chest into pieces up to the sensation of physical unbearable torment, as well as with a number of other equally unpleasant symptoms. nine0003

The key to such a disease is that it does not depend on external causes, which is why it is called endogenous. That's when the body, which inherited a failure of the genetic program, decides to once again upset its own balance of neurotransmitters and hormones, then the exacerbation will begin. Poverty can only indirectly affect the duration of such an exacerbation: for example, there is no money for medicines that are prescribed for preventive purposes. Directly, no, not at all.

Poverty can only indirectly affect the duration of such an exacerbation: for example, there is no money for medicines that are prescribed for preventive purposes. Directly, no, not at all.

Item two, reactive depression. nine0003

May present with the same symptoms and just as pronounced as endogenous. The difference is that the reactive one has a clear reason: after all, it develops as a reaction, and not just to stress, but to a personal disaster, tragedy. You understand, for this it is not enough just to earn less than a neighbor, or to find out that your salary has been cut. To do this, you have to lose everything. Or almost everything. Moreover, overnight or in a relatively short period of time. Are there many of these now? There is, of course, but not in the same way as it was in the nineties. nine0003

As for the third point, neurotic depression, or depressive syndrome in neurosis, here, yes, here, in order to get the debut of a neurosis or decompensation of an existing one, it is necessary that an unpleasant, stressful factor be not necessarily catastrophic, but act, undermining strength, quite long time.

And long-term lack of money can turn out to be just such a stressful factor. And indeed sometimes it turns out. Just something to take into account. Even in the presence of this very stressful factor, under other external conditions being equal, not every person will develop a neurosis. nine0003

Here, firstly, it is necessary to have a certain personality type, for which it is intrapersonal (oh, what a weakling I am, I don’t even know how to earn money!) you have to, all in the same place, with claims!) will be critically significant. And secondly, genes again. Predisposing to the development of neurosis.

Similar factory firmware on a phone or on-board computer of a car with preset settings. That is, there will be more neuroses arising from poverty than reactive and exacerbated endogenous depressions, but even if you add up all three points, the total amount will be much less than that which does not relate to something painful, has no right to be called depression and is represented fourth and last point. nine0003

nine0003

So, the fourth point. Bad mood.

Any psychologist will explain where it comes from in case of lack of money. There is a whole chain: need - motivation - action - emotion for a positive or negative result. Well, no one needs to justify the need for material well-being: too much is now tied to money. Motivation to raise the butt, and actions to get this money, also do not have to be painted. As well as emotions, negative in case it was not possible to earn money, or it was possible, but not enough. nine0003

We just completely forgot that negative emotions are not always something bad or painful.

Just here they are completely natural and justified. Moreover, normally they should serve as an initiating pendle for the individual: get up, do something! Find additional income, change your job, and if it doesn't work out, cut your sturgeon... sorry, needs and requests - and don't worry!

It's just that someone has managed to relax and wean himself from the fact that you first need to fight for the right of Blessed Dolce Far Niente.