Cause of baby boomers

Definition, Years, Date Range, Retirement & Preparation

What Is a Baby Boomer?

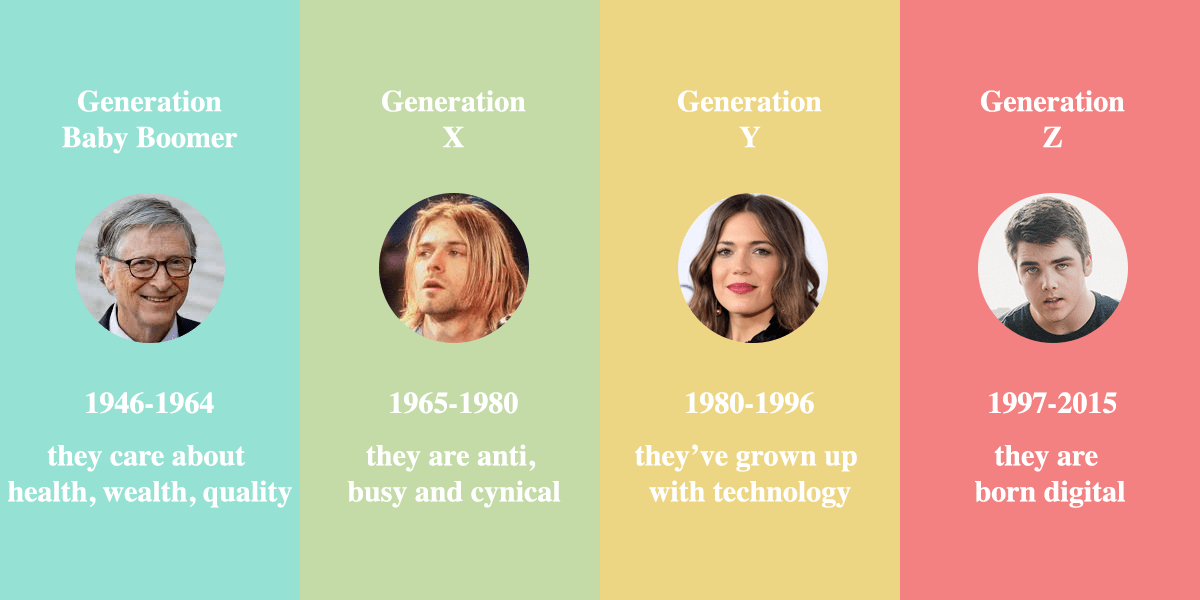

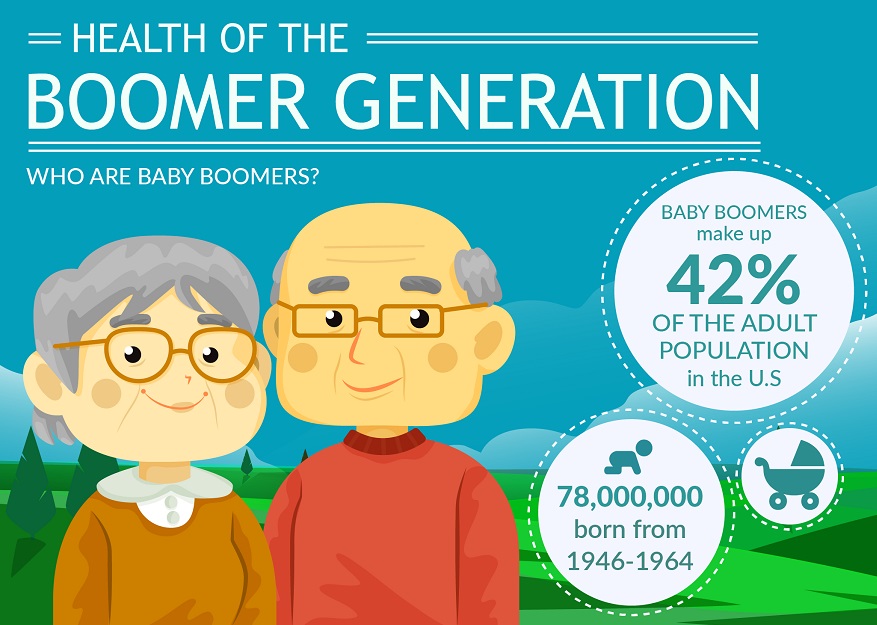

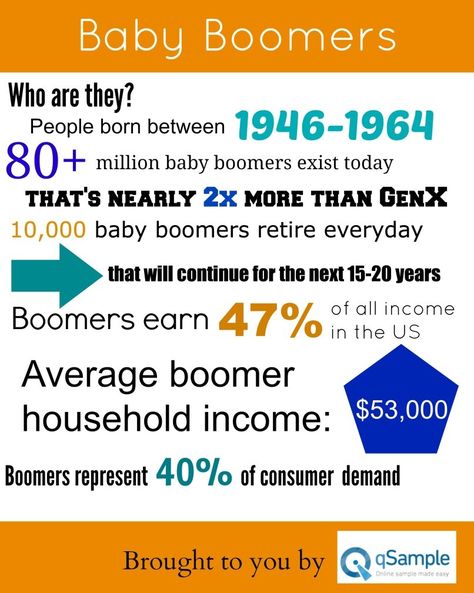

"Baby boomer" is a term used to describe a person who was born between 1946 and 1964. The baby boomer generation makes up a substantial portion of the world's population, especially in developed nations. According to the latest census report, it represents 73 million of the population in the United States, as of July 2019.

As the largest generational group in U.S. history (until the millennial generation slightly surpassed them), baby boomers have had—and continue to have—a significant impact on the economy. As a result, they are often the focus of marketing campaigns and business plans.

Key Takeaways

- "Baby boomer" refers to a member of the demographically large generation born between the end of WWII and the mid-1960s.

- Because of their high numbers and the relative prosperity of the U.S. economy during their careers, the baby boomers are an economically influential generation.

- Today, baby boomers are reaching retirement age and face some key challenges, including funding their retirements.

- The term "baby boomer" is derived from the boom in births that took place after the return of soldiers from WWII.

Baby Boomer

Understanding a Baby Boomer

Baby boomers emerged after the end of World War II when birth rates across the world spiked. The explosion of new infants became known as the baby boom. During the boom, 76 million babies were born in the United States alone.

Most historians say the baby boomer phenomenon most likely involved a combination of factors: people wanting to start the families that they put off during World War II and the Great Depression, and a sense of confidence that the coming era would be safe and prosperous. Indeed, the late 1940s and 1950s generally saw increases in wages, thriving businesses, and an increase in the variety and quantity of products for consumers.

Accompanying this new economic prosperity was a migration of young families from the cities to the suburbs. The G.I. Bill allowed returning military personnel to buy affordable homes in tracts around the edges of cities. This led to a suburban ethos of the ideal family comprised of the husband as the provider, the wife as a stay-at-home housekeeper, plus their children.

The G.I. Bill allowed returning military personnel to buy affordable homes in tracts around the edges of cities. This led to a suburban ethos of the ideal family comprised of the husband as the provider, the wife as a stay-at-home housekeeper, plus their children.

As suburban families began to use new forms of credit to purchase consumer goods such as cars, appliances, and television sets, businesses also targeted those children, the growing boomers, with marketing efforts. As the boomers approached adolescence, many became dissatisfied with this ethos and the consumer culture associated with it, which fueled the youth counterculture movement of the 1960s.

That huge cohort of children grew up to pay the decades of Social Security taxes that funded the retirements of their parents and grandparents. Now, millions each year are retiring themselves.

As the longest-living generation in history, boomers are at the forefront of what’s been called a longevity economy, whether they are generating income in the workforce or, in their turn, consuming the taxes of younger generations in the form of their Social Security checks.

By 2034, it is projected that older adults will outnumber those under age 18 for the first time in U.S. history.

In a 2021 article by the Brookings Institution, Baby boomers spent about $8.7 trillion in 2020 on goods and services. This is expected to increase to $15 trillion by 2030.

And even though they are aging (the very youngest boomers are in their late 50s as of 2021) they continue to hold corporate and economic power; in the U.S., 50.3% of personal net worth belongs to boomers.

Baby Boomers and Retirement: Why the Boomers' Retirement Is Different

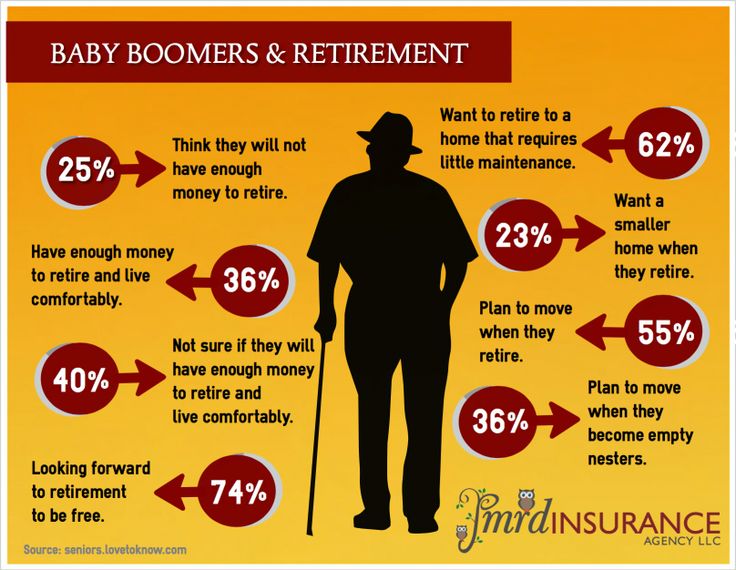

The first of the baby boom generation became eligible to retire in 2011. In many ways, the way they spend their post-work years will be different from that of their parents; members of what's often called the Greatest Generation.

Much Longer Retirement

Many people in previous generations worked as long as they could and few were fortunate enough to have a retirement that would be considered golden by today's standards. America's post-World War II prosperity made things better for the greatest generation, who benefited from a workforce in which there were over 16 employees for every retiree. Plenty of people in that generation were able to retire at the official age of 65.

America's post-World War II prosperity made things better for the greatest generation, who benefited from a workforce in which there were over 16 employees for every retiree. Plenty of people in that generation were able to retire at the official age of 65.

One change between then and now is that a large percentage of the 73 million American baby boomers are expected to live longer than their parents did. So their retirement period will be longer.

Higher Expectations

With more health and energy—and their children now adults—boomers who can afford it expect to spend at least early retirement fulfilling travel dreams and other bucket-list items. Those who reach retirement age now are often healthy enough to run marathons, build houses, and even start businesses.

Instead of relocating to retirement communities, many are migrating to small towns that can offer employment and education opportunities. Other boomers are choosing to move into urban areas to take advantage of amenities, such as public transportation and cultural attractions.

Some with thinner resources are retiring outside the U.S. to countries with lower costs of living, such as Mexico, Portugal, and the Philippines. Twenty-five percent have no retirement savings, according to the 2021 Retirement Readiness report of the Insured Retirement Institute.

More Investment Choices, Less Investment Safety

The greatest generation had relatively few investment options: mostly ordinary bonds and certificates of deposit. But those are relatively secure forms of income. That's not true for the boomers. What's more, with a longer lifespan comes more opportunity, and need, to take at least some investment risks to ensure keeping up with inflation.

Today's boomers are faced with an ever-expanding universe of income securities. The investment industry has provided a lot of rope to invest, and a lot of new and exciting ways to lose it all.

If they felt like taking a risk, the boomers' parents might have bought some dividend-paying stocks. At the time, most of the dividend-paying industries, such as finance and utilities, were highly regulated. Decades of deregulation have caused these industries to become less predictable and riskier. Hence, the certainty of previously assumed dividends or return on investments is now uncertain.

At the time, most of the dividend-paying industries, such as finance and utilities, were highly regulated. Decades of deregulation have caused these industries to become less predictable and riskier. Hence, the certainty of previously assumed dividends or return on investments is now uncertain.

Rising, Instead of Declining, Interest Rates

In the 1980s, when the greatest generation started to retire, interest rates exceeded 19%. This was good for savers (and terrible for homebuyers). Ever since, interest rates have been decreasing, with some periods of increases. For example, during the COVID-19, interest rates dropped to a target of 0% to 0.25% in March 2020 but rose two years later to target of 0.75% to 1% as of May 2022. The long decline in interest rates provided a great return to bond investors.

The boomers are facing the very opposite situation. Instead of an ever-declining interest rate, they are facing the likelihood of steadily increasing interest rates during their retirement.

Personal Savings Instead of Pensions

The greatest generation might have had a lower per capita income, but many of its members also had corporate or union pensions, which could be a considerable amount after working for a lifetime for the same employer, as was once common.

But the economy changed, many large corporations merged or disappeared, and unions dropped from 20.1% of workers in 1983 to 10.3% in 2019, according to the U.S. Bureau of Labor Statistics.

What's more, traditional corporate pensions have been largely phased out now, giving way to 401(k) plans, IRAs, and other investment vehicles that put the onus on saving on the individual. Because they were the first generation to encounter these changes, most boomers didn't start saving enough or early enough.

The IRS allows for increased contributions to retirement accounts for those age 50 and older, known as "catch-up contributions."

As for the federal pension known as Social Security, there is concern that it could fall short. The problem is that the baby boomer generation is much larger than previous generations; Generation X, which follows it, is much smaller; and even the larger-than-the-boomers millennial generation isn't large enough to offset the increased longevity of boomers.

The problem is that the baby boomer generation is much larger than previous generations; Generation X, which follows it, is much smaller; and even the larger-than-the-boomers millennial generation isn't large enough to offset the increased longevity of boomers.

Unless there are changes in how Social Security is structured, estimates are that there will not be enough tax-paying workers to support full Social Security payments to the retiree population, starting in 2034. During the years baby boomers began joining the workforce, the ratio of workers to retirees ranged from 5.1 to 3.3, approximately. As of 2013, that number fell to 2.8 and is expected to decrease.

A Retirement Fund Shortage?

In addition to many not saving enough money, boomers experienced the Great Recession at a crucial time for their retirement savings. Many boomers jumped into expensive investments, mortgages, and startups in the late 1990s, only to find themselves struggling to make those payments a few years later; many found themselves completely tapped out or their mortgages underwater.

The subprime meltdown of 2008 in the mortgage industry and the following stock market crash left many boomers scrambling to piece together an adequate nest egg. Many of them subsequently turned to borrowing against the equity in their homes as a solution. While real estate prices rose again, some boomers still can't profit substantially from selling their current home in order to find a cheaper one.

For those with such debts, savings have been put on the back burner. What's more, boomers who responded to the Great Recession by turning ultra-conservative with the savings they had left got a second hit: By not holding enough of their portfolios in stocks, they’ve missed the huge bull market that followed and risked letting their nest eggs stagnate. Meanwhile, wages have not increased significantly for many parts of the population.

How Boomers Can Prep for Retirement

Taking some of these steps could help baby boomers manage retirement.

Don't Retire (At Least Not Too Soon)

One idea might be the most non-traditional of all: don't retire. Or at least, delay doing so beyond the proverbial age 65, 66, or 67 (depending on birth date). Whether that means working longer, consulting, or finding a part-time gig, being part of the workforce can help boomers financially and emotionally.

Or at least, delay doing so beyond the proverbial age 65, 66, or 67 (depending on birth date). Whether that means working longer, consulting, or finding a part-time gig, being part of the workforce can help boomers financially and emotionally.

Finances permitting, boomers could also wait to take their Social Security benefits until they reach age 70. By postponing benefits, they can receive 132% of their original monthly stipend. This, combined with the increased income and savings from continuing to work will ease retirement.

Plan for Health Issues

Boomers, who came of age during the freewheeling 1960s and 1970s, often project an image that they will stay active forever; and indeed, many are in better shape than their forebears at the same age. Still, the human body isn't invulnerable. Obesity, diabetes, hypertension, and high cholesterol are inevitably all on the rise in the boomer population. Cancer and heart disease are the leading cause of death. And then there's dementia: according to the Institute for Dementia Research & Prevention, it is estimated that 1 in 6 women and 1 in 10 men who live past the age of 55 will develop dementia in their lifetime.

Make a Will

As of May 2020, 45% of adult Americans have a living will, which details their medical wishes, such as whether to be put on life support should they become unable to articulate their wishes. About 26% of boomers over 65 have not drawn up wills that stipulate how their assets should be distributed in the event of their own deaths, leaving the door open for a host of potential legal and financial problems.

The eldest boomers are still in their early 70s. That's the time to make decisions about healthcare and also about who should be in charge of their life and finances, should they be unable to make responsible decisions due to illness or incapacity. Boomers shouldn't leave those decisions to others; they should make them themselves.

It's also wise to look into long-term care insurance and other alternatives to paying for care in advanced old age. This is especially useful for younger boomers, for whom it will be less expensive.

Baby Boomers - What Caused The Baby Boom? - Age, Social, Fertility, and Income

There is no consensus regarding the cause of the baby boom: social scientists suggest a complex mixture of economic, social, and psychological factors. The majority of it occurred not through an increase in family size but rather through a sharp decline in the proportion of women choosing to remain childless (Westoff). For many older women these were births postponed during the Depression and World War II. They account for most of the immediate 1946– 1947 "spike" in births associated with returning Figure 1 A comparison of the historic U.S. birth rate and numbers of births in the United States. (Total Fertility Rate [TFR] is the number of births a woman would experience throughout her childbearing years, at current age-specific rates.) SOURCE: Vital Statistics and Natality, various years. troops at the end of the war. But in addition younger women departed from a historic upward trend in female labor force participation in order to stay home and start families—a departure that lasted for nearly twenty years. Exhilaration and optimism after the war seemed to combine with a general feeling of affluence in a booming postwar economy, and generous provisions for returning GIs, to make young couples feel able and willing to support children (Bean; Jones).

The majority of it occurred not through an increase in family size but rather through a sharp decline in the proportion of women choosing to remain childless (Westoff). For many older women these were births postponed during the Depression and World War II. They account for most of the immediate 1946– 1947 "spike" in births associated with returning Figure 1 A comparison of the historic U.S. birth rate and numbers of births in the United States. (Total Fertility Rate [TFR] is the number of births a woman would experience throughout her childbearing years, at current age-specific rates.) SOURCE: Vital Statistics and Natality, various years. troops at the end of the war. But in addition younger women departed from a historic upward trend in female labor force participation in order to stay home and start families—a departure that lasted for nearly twenty years. Exhilaration and optimism after the war seemed to combine with a general feeling of affluence in a booming postwar economy, and generous provisions for returning GIs, to make young couples feel able and willing to support children (Bean; Jones).

But this apparently positive relationship between income and fertility fails to explain why fertility rates then suddenly plummeted in the early 1960s, causing the "baby bust." There was a tendency at the time to attribute the decline to the introduction of the birth control pill in 1963—but it is generally acknowledged now that the pill merely facilitated a trend that originated several years earlier, in the late 1950s. Economists have attempted to develop a "unified theory" to explain both the boom and bust. Their focus has been primarily on three factors: male income, the female wage, and material aspirations (desired standard of living). They assume that fertility will tend to rise as male income rises, but fall when material aspirations increase and when female wages rise. The female wage is assumed to represent the value of time foregone in the labor market in favor of childbearing: the "opportunity cost" or "price" of women's time Figure 2 A comparison of baby booms in several western nations using the Total Fertility Rate (TFR, which equals the number of births a woman would experience throughout her childbearing years, at current age-specific rates). The "official" baby boom years are indicated (1946–1964), and the dashed line marks a TFR of 2.1, which is replacement-level fertility. SOURCE: Author spent in caring for children and hence a significant element in the cost of raising children.

The "official" baby boom years are indicated (1946–1964), and the dashed line marks a TFR of 2.1, which is replacement-level fertility. SOURCE: Author spent in caring for children and hence a significant element in the cost of raising children.

One school of economic thought suggests that the baby boom in the 1950s was caused by rising male incomes and falling women's wages (as women were displaced from wartime jobs), while in the later decades falling male income and rising female wages generated the baby bust (Butz and Ward). Unfortunately data needed to test this hypothesis fully are not available for the complete boom—and bust—period although the data that are available suggest that these two factors account for only a portion of the baby boom (and bust).

However, adding the third factor—material aspirations—provides a more complete explanation for the phenomenon. This third factor has been the focus of another school of thought among economists, which assumes that shifts over time in the desired standard of living temper young adults' responses to intergenerational changes in income. That is, it is assumed that young adults will feel affluent only if their income—regardless of its absolute level—allows them to meet or exceed their material aspirations, which are assumed to be in large part a function of the standard of living they experienced while growing up (Easterlin). And a couple's ability to achieve a given standard of living is affected by the size of their birth cohort relative to that of their parents. An excess supply of younger, less-experienced workers depresses their wages relative to older workers, and excess demand produces the opposite result (Welch; Macunovich, 1999). Since those older workers are the parents of the young adults, and are assumed to affect their children's desired standard of living, it is assumed that large cohorts will have a difficult time achieving their material aspirations—and conversely small cohorts will be favored.

That is, it is assumed that young adults will feel affluent only if their income—regardless of its absolute level—allows them to meet or exceed their material aspirations, which are assumed to be in large part a function of the standard of living they experienced while growing up (Easterlin). And a couple's ability to achieve a given standard of living is affected by the size of their birth cohort relative to that of their parents. An excess supply of younger, less-experienced workers depresses their wages relative to older workers, and excess demand produces the opposite result (Welch; Macunovich, 1999). Since those older workers are the parents of the young adults, and are assumed to affect their children's desired standard of living, it is assumed that large cohorts will have a difficult time achieving their material aspirations—and conversely small cohorts will be favored.

This economic approach assumes that the fertility cycle experienced between 1936 and 1976 was one of the demographic adjustments young adults made in response to "relative cohort size"–induced changes in "relative income. " It suggests that the small cohorts born during the Depression entered the labor market in the 1950s with relatively low material aspirations and found themselves favored not only by the strong economy but also by their small relative cohort size. Their high relative income generated the baby boom, but when the boomers themselves entered the labor market in the 1970s and 1980s their experience was diametrically opposed to that of their parents: high material aspirations coming out of their parents' homes, but low earnings relative to those expectations thanks to their large cohort size. The boomers' fertility rates plummeted as they scrambled to maintain their desired standard of living (Macunovich, 1998).

" It suggests that the small cohorts born during the Depression entered the labor market in the 1950s with relatively low material aspirations and found themselves favored not only by the strong economy but also by their small relative cohort size. Their high relative income generated the baby boom, but when the boomers themselves entered the labor market in the 1970s and 1980s their experience was diametrically opposed to that of their parents: high material aspirations coming out of their parents' homes, but low earnings relative to those expectations thanks to their large cohort size. The boomers' fertility rates plummeted as they scrambled to maintain their desired standard of living (Macunovich, 1998).

At the same time, the large American army was about to return to normal life. The combination of these factors threatened the American economy with a colossal collapse. Truman carried out the demobilization in the shortest possible time, so that the military could return to their families as soon as possible. At the same time, he was in no hurry to abolish centralized regulation in the economy, realizing that only in this way the federal government was able to counteract hidden threats on the path to development. The head of state extended current contracts, reduced government oversight of prices and wages, and was about to wait for results. nine0003

At the same time, the large American army was about to return to normal life. The combination of these factors threatened the American economy with a colossal collapse. Truman carried out the demobilization in the shortest possible time, so that the military could return to their families as soon as possible. At the same time, he was in no hurry to abolish centralized regulation in the economy, realizing that only in this way the federal government was able to counteract hidden threats on the path to development. The head of state extended current contracts, reduced government oversight of prices and wages, and was about to wait for results. nine0003

Gasoline consumers

But the results were excellent. As it turned out, the Americans accumulated $140 billion worth of savings during the war, and they wanted to spend them on scarce goods. The people agreed to spend money, but, alas, a new problem soon surfaced: a shortage of the required goods, an increase in prices for consumer goods and mass protests organized by specialized trade unions. The president's steps in the economic industry (sometimes not very successful) provoked legitimate irritation of the population. nine0003

The president's steps in the economic industry (sometimes not very successful) provoked legitimate irritation of the population. nine0003

So, the soldiers were returning home from the war. The decade was coming to an end, and the situation began to gradually improve. Now the Americans could allow themselves those pleasures in which they had previously infringed upon themselves. Since 1946, the birth rate in the state has increased immediately, accompanying (to a large extent and pushing) economic expansion. Scientists began to talk about a population explosion. Judge for yourself: if during the 1930s population growth reached about 7%, in 19In the 1940s, it reached 15%. And in the 1950s, this level already reached almost 20%; decreased slightly in the 1960s, but still remained at around 13%. In addition, most of the growth was produced through high birth rates. The peak fell on 1957, when more than 4 million babies saw the world - that is, one newborn every 7 seconds. While Europe saw only a short-term increase in the birth rate in the first post-war period, America witnessed an incredible phenomenon, when for two decades the nation experienced an uninterrupted "baby boom". nine0003

nine0003

Having received extra money and large families, Americans have changed their own idea - not only about how to spend life, but also where to equip housing. In the years 1940-1970, there was an outflow of population from large cities: only 1/3 of Americans remained to live there. The proportion of the rural population has also fallen to over 30 percent. At the same time, the number of those who preferred to settle on the outskirts of large cities increased significantly: if earlier they accounted for only 20% of the total population of the country, now this figure has reached 33%. So, the "boom" took place in another area of life - in the development of numerous suburbs. nine0003

In the decades after the end of the war, the geography of the settlement of residents also changed: in the west, south and south-west of the country, a kind of “sunny belt” was formed. While the population of New York more or less stabilized, and such settlements as Chicago, Philadelphia and Boston even decreased, the number of residents of Los Angeles, Dallas, Atlanta, Phoenix, and Miami inevitably increased. In 1950, Los Angeles was the fourth most populated American city, with 19In 70 he moved to third place, and in 1990 he was already in second place. Since the early 1960s, New York State is no longer the most populous state in America and has lost that title to California.

In 1950, Los Angeles was the fourth most populated American city, with 19In 70 he moved to third place, and in 1990 he was already in second place. Since the early 1960s, New York State is no longer the most populous state in America and has lost that title to California.

The post-war period was marked by incredible economic growth. Between 1945 and 1950, the total size of goods and services manufactured in the United States increased by almost 25%. US GNP rose sharply by 80% in the 1950s, then by 83% in the 1960s, and by almost 150% in the 1970s. From 1945 to 1980, GNP increased more than eleven times. Gone are the days when profits were completely eaten up by increased prices. In the period 1945-1960, the true (including with inflation) price of manufactured products rose by 55%. So in the "inflationary" 1960-1970s, the US GNP more than doubled.

Baby Boomer - Financial Encyclopedia

What is a Baby Boomer?

Baby boomer is a term used to describe a person born between 1946 and 1964. The baby boomer generation makes up a significant portion of the world's population, especially in developed countries. He represents nearly 20% of the American public. nine0003

The baby boomer generation makes up a significant portion of the world's population, especially in developed countries. He represents nearly 20% of the American public. nine0003

As the largest generational group in US history (until the Millennials slightly surpassed them), the Baby Boomers had – and continue to have – a significant impact on the economy. As a result, they are often the subject of marketing campaigns and business plans.

Highlights

- Baby Boomer refers to a member of the demographically large generation born between the end of World War II and the mid-1960s.

- Because of their numbers and the relative prosperity of the US economy during their careers, the Baby Boomers have become an economically powerful generation. nine0034

- Today, baby boomers are approaching retirement age and are facing some key challenges, including funding their pensions.

The history of baby boomers

Baby boomers appeared after the end of World War II, when the birth rate around the world skyrocketed.![]() The explosion of newborns became known as the baby boom. During the boom, nearly 77 million babies were born in the United States alone, representing nearly 40% of the American population.

The explosion of newborns became known as the baby boom. During the boom, nearly 77 million babies were born in the United States alone, representing nearly 40% of the American population.

Most historians say that the baby boomer phenomenon was most likely due to a combination of factors: people wanted to start families, which they put off during World War II and the Great Depression, and a sense of confidence that the coming era would be safe and prosperous. Indeed, at the end of 19The 1940s and 1950s generally saw rising wages, flourishing businesses, and an increase in the variety and quantity of goods available to consumers.

This new economic prosperity was accompanied by the migration of young families from the cities to the suburbs. The GI Bill allowed returning military personnel to buy affordable housing in tracts along the edges of cities. This led to the formation of an ideal family, consisting of a husband as a breadwinner, a wife as a housekeeper and their children.

As suburban families began to use new forms of credit to buy consumer goods such as cars, appliances and televisions, companies also targeted these rising boomers through marketing efforts. As boomers approached adolescence, many became dissatisfied with this ethos and the associated consumer culture that fueled the youth counterculture movement.60s.

This huge group of children grew up to pay 10 years of Social Security taxes that covered their parents' and grandparents' pensions. Millions of people are now retiring every year.

As the longest living generation in history, Boomers are at the forefront of what is called the longevity economy, whether they generate income in the form of labor or, in turn, consume the younger generation's taxes in the form of their Social Security checks. . nine0003

According to a recent AARP Bulletin, Baby Boomers spend $7 trillion a year on goods and services. And even though they are aging (the youngest boomers in 2019 are already over 50), they still have corporate and economic power - 80% of the country's personal wealth belongs to boomers.

Baby boomers and retirement age: why the retirement age of baby boomers is different In many ways, how they spend their postpartum years will be different from that of their parents, members of what is often referred to as the Greatest Generation. nine0003

A much longer pension

Many people in previous generations worked as hard as they could, and only a few were lucky enough to have a pension that would be considered golden by today's standards. America's post-World War II prosperity improved the fortunes of the Greatest Generation, which benefited from a workforce of six for every retiree. Many people of this generation were able to retire at the age of 65.

There has been one change since then: a large percentage of America's 77 million baby boomers are expected to live 10 to 25 years longer than their parents. Those who retire at age 60 can expect to live at least 25 more years. So they will have a longer retirement period. nine0003

Higher expectations

With greater health and energy—and their children growing up—boomers who can afford it expect to spend at least an early retirement, fulfilling travel dreams and other important affairs. Those now reaching retirement age are often healthy enough to run marathons, build houses, and even start businesses.

Those now reaching retirement age are often healthy enough to run marathons, build houses, and even start businesses.

Instead of moving to retirement communities, many are migrating to smaller towns where there are opportunities for work and education. Other boomers choose to move to urban areas to enjoy amenities such as public transportation and cultural attractions. nine0003

Some of them, with more limited resources, are retiring outside the US to countries with a lower cost of living, such as Mexico, Portugal, and the Philippines. Forty-five percent have no retirement savings, according to a 2019 report from the Insured Pensions Institute.

More investment opportunities, less investment security

The largest generation had relatively few investment options: mostly conventional bonds and certificates of deposit. But these are relatively safe forms of income. This is not true for boomers. Moreover, as life expectancy increases, there are more opportunities and the need to take on at least some investment risk in order to keep up with inflation. nine0003

nine0003

Exotic investment opportunities

Today's boomers face an ever-expanding universe of income securities. The investment industry has provided many investing opportunities and many exciting new ways to lose it all.

Deregulation

If they were willing to take the risk, Baby Boomer parents might have bought some dividend-paying stock. At the time, most dividend-paying industries, such as finance and utilities, were heavily regulated. Decades of deregulation have made these industries less predictable and more risky. Therefore, the reliability of a previously anticipated dividend or return on investment is currently uncertain. nine0003

Raise, not cut interest rates

In the 1980s, when the largest generation began to retire, interest rates were around 18%. It was good for the budget conscious (and terrible for homebuyers). In 2010, rates were about as low as they are, less than 1%. This continued decline in interest rates provided large returns for bond investors.

Boomers found themselves in a completely opposite situation. Instead of constantly decreasing interest rates, they face the possibility of constantly increasing interest rates during retirement. nine0003

Personal savings instead of pensions

The top generation could have had a lower 10.5% in 2018, according to the US Bureau of Labor Statistics. What's more, traditional corporate pensions are now largely phased out, giving way to 401(k) plans, IRAs, and other investment vehicles that place the burden of savings on individuals. Because they were the first generation to experience these changes, most boomers didn't start saving enough or early. nine0003

With regard to the federal pension, known as Social Security, there are concerns that it may not be sufficient. The problem is that the baby boomer generation is much larger than previous generations; Generation X that follows is much smaller; and even the millennial generation, which is larger than those who grew up as a result of the economic boom, is not large enough to compensate for the increase in boomer life expectancy.

Unless changes are made to the structure of social security, it is estimated that there will not be enough tax-paying workers to provide full social security payments to pensioners starting in 2034. Back in the years when baby boomers were in the workforce, there were six employees for every retiree. But it is estimated that by the time the entire baby boomer generation reaches retirement age, that ratio will drop to three to one. nine0003

Pension fund shortage?

In addition to the fact that many of them do not save enough money, the Boomers survived the Great Recession at a critical time for their retirement savings. Many boomers threw themselves into high-priced investments, mortgages, and startups in the late 1990s, only to find it difficult to make these payments after a few years; many found themselves completely disabled or lost their mortgages.

The sub-major crash of 2008 in the mortgage industry and the following stock market crash left many boomers scrambling to put together a sufficient nest egg. Many of them subsequently turned to equity borrowing as a solution to the problem. Even though real estate prices are starting to rise again, some people who are experiencing a period of economic boom still cannot make a substantial profit from selling their current home in order to find a cheaper one. nine0003

Many of them subsequently turned to equity borrowing as a solution to the problem. Even though real estate prices are starting to rise again, some people who are experiencing a period of economic boom still cannot make a substantial profit from selling their current home in order to find a cheaper one. nine0003

For those who have such debts, the savings are put on the back burner. What's more, the boomers who reacted to the Great Recession by turning into ultra-conservatives with their savings left over suffered a second blow: by not holding enough of their portfolios in stocks, they missed out on the huge bull market that followed and risked letting their eggs in the nest stagnate. . Meanwhile, for many segments of the population, wages did not rise significantly.

How boomers can prepare for retirement

Some of these steps can help baby boomers to retire.

Don't retire (at least not too soon)

One idea might be the most unconventional: don't retire. Or at least postpone it until proverbial age 65 or 66 (depending on date of birth). Whether that means longer hours, counseling, or finding part-time jobs, being in the workforce can help boomers financially and emotionally. nine0003

Or at least postpone it until proverbial age 65 or 66 (depending on date of birth). Whether that means longer hours, counseling, or finding part-time jobs, being in the workforce can help boomers financially and emotionally. nine0003

If finances permit, boomers can also wait until they are 70 to receive Social Security benefits. By delaying their benefits, they can receive 132% of their original monthly stipend. This, combined with increased income and savings from continuing to work, will make retirement easier.

Health plan

Boomers who came of age in the free 1960s and 1970s often create the image that they will stay active forever—indeed, many of them are in better shape than their ancestors in the same age. However, the human body is not invulnerable. Obesity, diabetes, hypertension, and high cholesterol are inevitably on the rise in the boomer population. Cancer and heart disease are the main causes of death. And then there's dementia: According to the Institute for Dementia Research and Prevention, it's estimated that one in six women and one in ten men who live to age 55 will develop dementia during their lifetime.